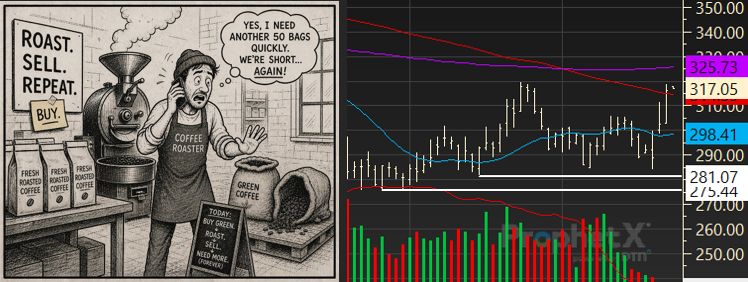

KC K26: 290.90 – 316.35

K26 / N26: 5.80 – 16.00

Market levels referenced in this update reflect conditions as of April 24, 2026.

Pricing Week: First Notice Day Pressure

It didn’t take long this week for fireworks to start in the market. Heading into FND (First Notice Day), the last day for roasters to price coffees for April and May deliveries, it became clear that many participants were hoping the market would break below 290, or even the recent lows near 281 (4/8/26 and 3/16/26) or 275 (2/24/26). On Tuesday, the market dipped to 284.20, sparking buying. That buying sparked more buying as shorts (roasters and the trade) were forced to pay up to cover. The race to recent highs was on, with Thursday’s close settling just above the 100-day moving average at 316.35.

Nothing new here. We’ve seen it time and again over the past few years as roasters and the trade have wrestled with how to operate in an inverted market. Backwardation, almost by definition, means higher flat prices, driven by a general lack of supply. For roasters, relief from higher prices always feels just over the horizon. For the trade, the spread, or the cost arbitrage between contracts, always feels too high. So both sit and wait. Then, as time runs out and the game of chicken plays out, trade shorts and roasters alike have to step in and buy the nearby contract month. Roasters, to price their contracts, and importers, carrying long physical positions, to roll their hedge.